First Direct lives in its own little corner of UK banking. It’s the closest thing we have to a fintech built on top of a traditional high‑street bank: a fast, modern app, excellent customer service, fee‑free spending abroad, and access to HSBC branches and cash deposits. On paper, it looks like the perfect current account.

But for all the things it gets right, I don’t use First Direct as my main bank. Not because anything is wrong — far from it — but because it isn’t the best fit for everything I need a bank to do.

Quick Verdict

Best for: People who want a clean, fast banking experience with excellent customer service and access to cash deposits.

Avoid if: You prioritise cashback, premium credit cards, spending insights, or market-leading savings rates.

Monthly fee: Free

App quality: Excellent

Cash deposits: Outstanding

Web app: Decent

Savings rates: Mixed

Customer support: Excellent

Pros

- One of the fastest banking apps in the UK

- Excellent customer service

- Fee-free spending abroad

- Easy cash deposits through HSBC branches and the Post Office

- A clean, distraction-free experience

- Strong regular saver account

Cons

- Weak everyday savings rates

- A very basic credit card offering

- Spending insights that lag behind Monzo and Starling

- Limited customisation within the app

- No Open Banking support

- No virtual cards

Opening the Account

Opening the account was refreshingly simple. The whole process took only a few minutes, with approval arriving almost immediately. My debit card was ready for Apple Wallet straightaway, so I could start using the account before the physical card had even arrived.

First Direct did run a hard credit search, which showed up on my TransUnion report almost instantly. Other than that, the onboarding was about as smooth as banking gets. No friction. No confusing steps. Just a current account ready to use.

App Experience

This is where First Direct stands apart. While Monzo and Starling keep adding features, widgets, and budgeting tools, First Direct has gone in the opposite direction. The app is almost aggressively simple: black and white, no banners, no promotions, no nudges.

You open it, check your balance, make a payment, and close it again — and that’s the point. Everything loads instantly and navigation is effortless.

The only area where the app falls behind is spending insights. Transfers count towards spending totals, which makes the data far less useful if you regularly move money between accounts. The visual presentation is nice enough, but it’s miles behind Monzo and Starling.

Card controls are straightforward, login is smooth, and First Direct seems to have toned down much of the security theatre traditionally associated with HSBC.

Everyday Banking Features

For most people, everyday banking isn’t about endless features — it’s about whether the basics work reliably. First Direct handles the fundamentals extremely well. Transfers are fast, direct debits behave as expected, Apple Pay and Google Wallet are fully supported, and managing your debit card is simple.

Fee‑free spending abroad remains a genuine advantage, especially as some banks have started to scale back their travel perks.

Then there’s customer support. This is the feature First Direct is most famous for. Calls are answered quickly, the staff are helpful, and the whole experience feels refreshingly human in an era where many banks hide behind chatbots.

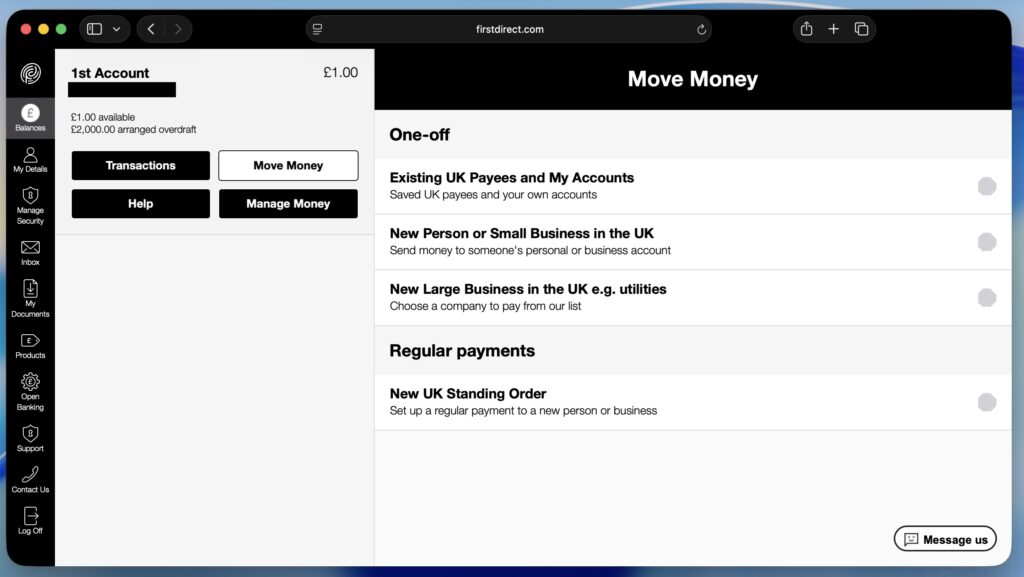

Web Access

Unlike Monzo and Chase, First Direct offers fully functional web access. Most people bank on their phones, but a proper web app is still incredibly useful: you can see more transactions at once, absorb more data on a larger screen, manage multiple tasks, download statements directly to your computer, and — the obvious one — keep going when your phone is out of battery.

It also gives the bank a sense of grounding. A service feels more “real” when it exists beyond the phone. (Hope I’m not showing my age here!)

So how is First Direct’s web app? Exactly as you’d expect. Quick, functional, and very Black & White. Everything works just as it does on the phone. It won’t win any design awards, but it’s a pleasure to use. You still need your phone to log in — you generate a Security Code in the app — but once you’re in, it’s solid.

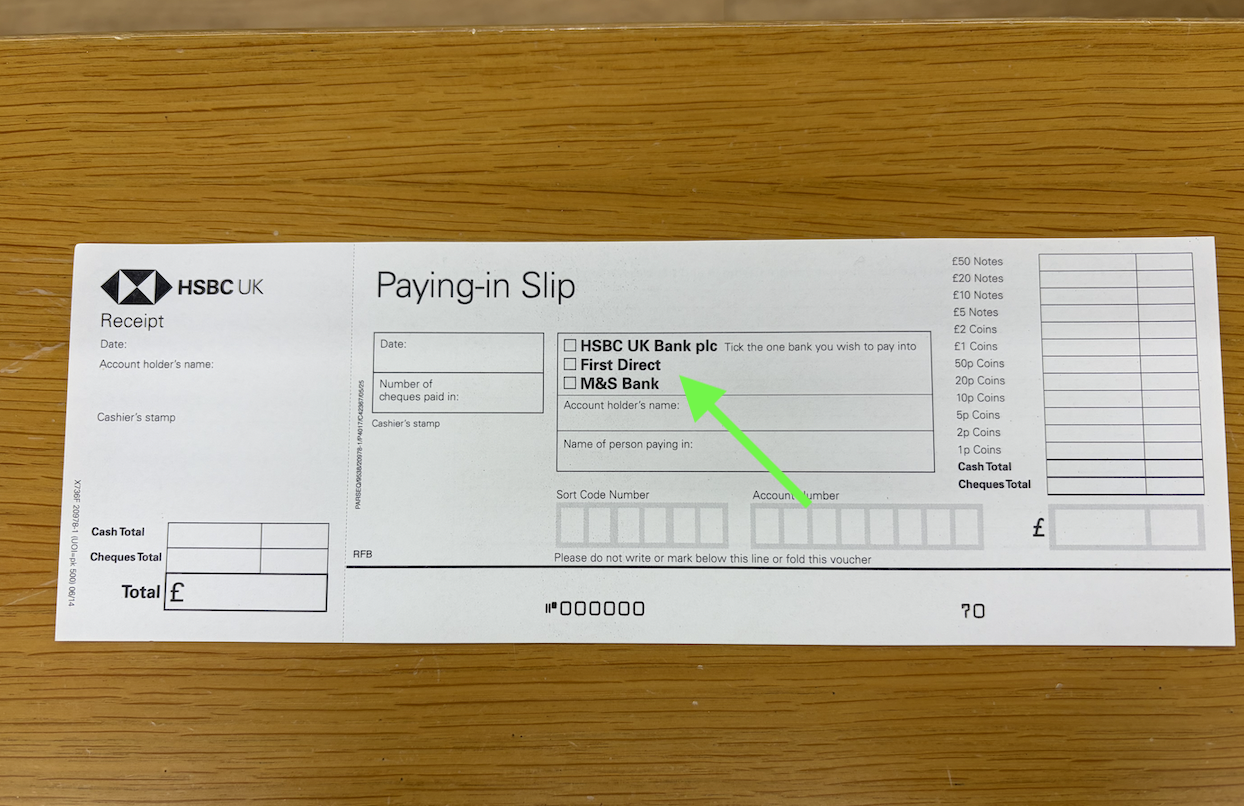

Cash Handling

This is where First Direct separates itself from most digital banks. Cash isn’t something I use regularly, but when you need it, you really need it. Because First Direct is backed by HSBC, customers can deposit cash at HSBC branches as well as through the Post Office network. For anyone who occasionally receives cash payments or simply likes having the option available, this is a significant advantage.

Monzo charges £1 per cash deposit. Starling allows deposits through the Post Office but charges 0.7% on deposits above £1,000 per year. Chase doesn’t support cash deposits at all. First Direct quietly avoids all of these limitations.

For some people, that won’t matter. For others, it’s the deciding factor.

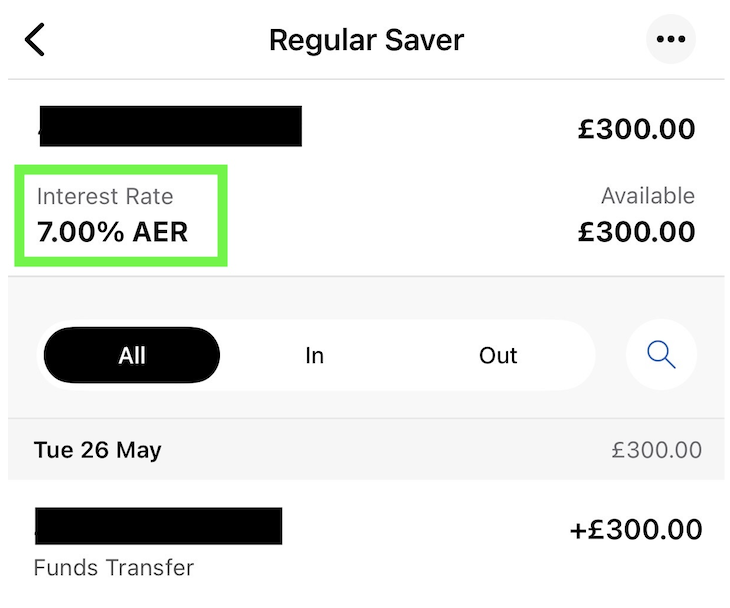

Savings & Interest

This is where the First Direct proposition starts to weaken. The savings products feel oddly disconnected from the quality of the current account.

At the time of writing, First Direct offers:

- Standard Saver: 1.05%

- Bonus Saver: 3.35%

- Regular Saver: 7%

The Standard Saver is difficult to recommend. With easy‑access accounts elsewhere paying well over 4%, there’s no reason to accept 1.05%.

The Bonus Saver is more interesting on paper, but the conditions undermine it. One withdrawal in a month and the rate drops back to 1.05%. It’s hard to see who this account is designed for when other providers offer better rates without the need to micromanage withdrawals.

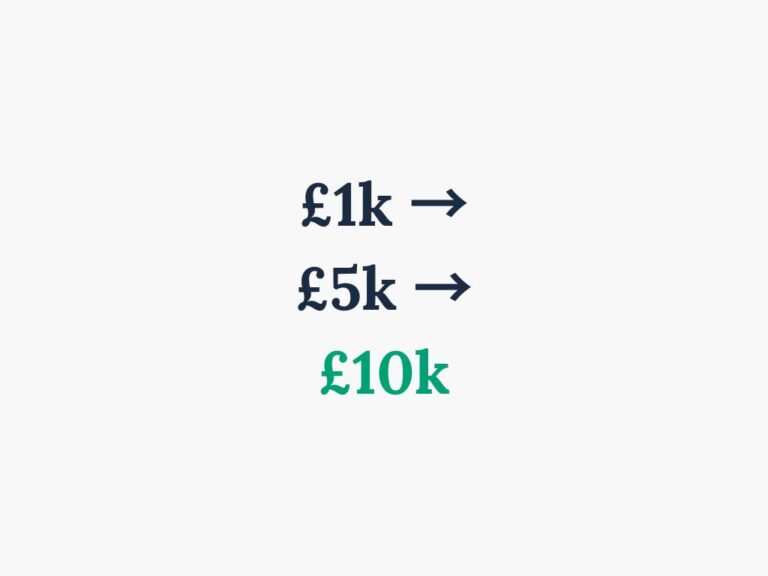

The Regular Saver, however, is excellent — one of the best products First Direct offers. The 7% headline rate understandably attracts attention, though it’s worth remembering how regular savers work: you only earn interest on each monthly deposit for the time it remains in the account, so the real return is lower than the headline suggests.

Even so, it’s a genuinely strong product. And unlike the Bonus Saver, the restrictions make sense. The account rewards consistent monthly saving, which is exactly what it’s designed to do.ing consistent monthly saving, which is exactly what the account is designed for.

Fees & Charges

One thing I genuinely appreciate about First Direct is how uncomplicated the fee structure is — it basically doesn’t exist.

There are no premium tiers, no subscription plans, and no hidden upgrades waiting to be sold later. The account is simply free.

Key charges include:

- Monthly fee: £0

- Foreign transaction fees: £0

- ATM fees: £0

- Replacement card fee: £0

- Cash deposit fees: £0

First Direct also offers an interest‑free overdraft buffer on the first £250, which is a welcome addition. It’s difficult to find fault here.First Direct also offers an interest‑free overdraft buffer on the first £250, which is a welcome addition. It’s difficult to find fault here.

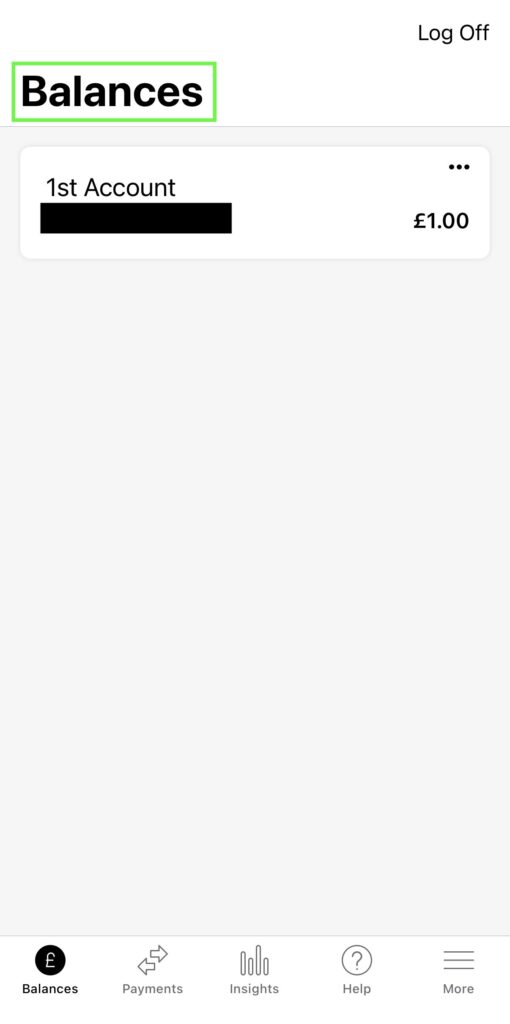

The Limits of Simplicity

First Direct’s simplicity is both its defining strength and its biggest limitation. Compared with Monzo and Starling, there aren’t many tools for organising money. There’s no Open Banking, no virtual cards, and you can’t rename or reorder accounts. Even the homepage avoids small‑talk and simply shows Balances. It feels like a throwback to when banking apps weren’t trying to be super‑apps — and First Direct seems perfectly comfortable with that.

Whether that’s a problem depends entirely on what you need. If you want advanced budgeting, customisation, or modern add‑ons, you’ll need to look elsewhere. First Direct is, in many ways, the “anti‑Monzo”: a bank that stays out of your way rather than trying to become the centre of your financial life. For some people, that’s a limitation. For others, it’s the whole appeal.

Final Verdict

Most people choose a bank by asking, “What’s the best account in the UK?” or “Can this account do everything?” I think the better question is, “What job do I need this account to do?” If you want cashback, rewards, premium credit cards, advanced budgeting tools, or market‑leading savings rates, First Direct probably isn’t the best choice — other banks simply offer more.

But if you want a fast, reliable account that quietly handles the basics of your financial life, First Direct is genuinely excellent. That’s how I use it: salary arrives, money moves to savings and investments, bills get paid, everything works, and the app stays out of the way.

For me, that makes it the best “money manager” account in the UK.