I genuinely love the First Direct app.

The black‑and‑white look, the quietness, the speed — it all feels refreshingly simple. No gimmicks, no noise, no one’s trying to sell you a holiday or some insurance product every time you log on.

I opened an account in about three minutes. Everything worked instantly. My card was already in Apple Wallet, payments arrived within seconds, and the app loaded immediately.

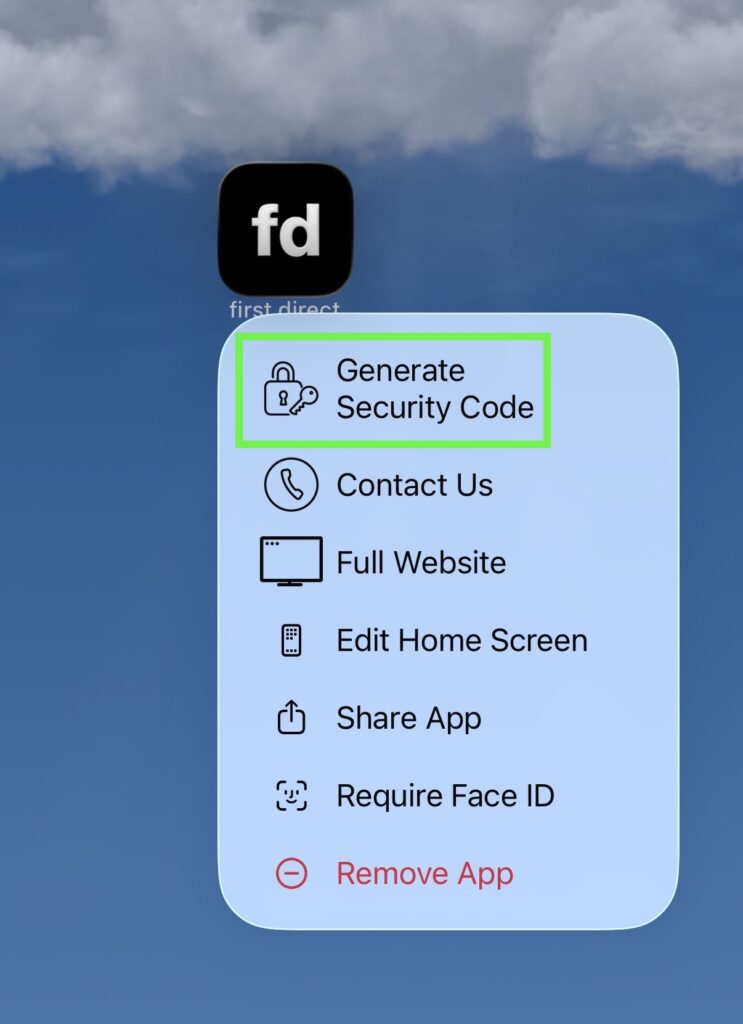

And here’s something most fintechs don’t offer: full web access. With First Direct you just generate a Security Code in the app and you’re straight in.

So at first glance, it seems to have the best of both worlds. But despite all that, I don’t actually think First Direct should be your main bank.

Here’s why.

The problems

For all its polish, First Direct still has some fairly major gaps:

- Savings rates aren’t competitive enough at 1.05% and 3.35% (bonus saver)

- The credit card offering is weak — no travel card, cashback, or rewards.

- First Direct Perks are pretty underwhelming, compared with Barclays, Lloyds and Monzo

- Spending insights are delayed and often inaccurate

So if you’re looking for the best place to save, invest, borrow, or optimise rewards, there are better options almost everywhere.

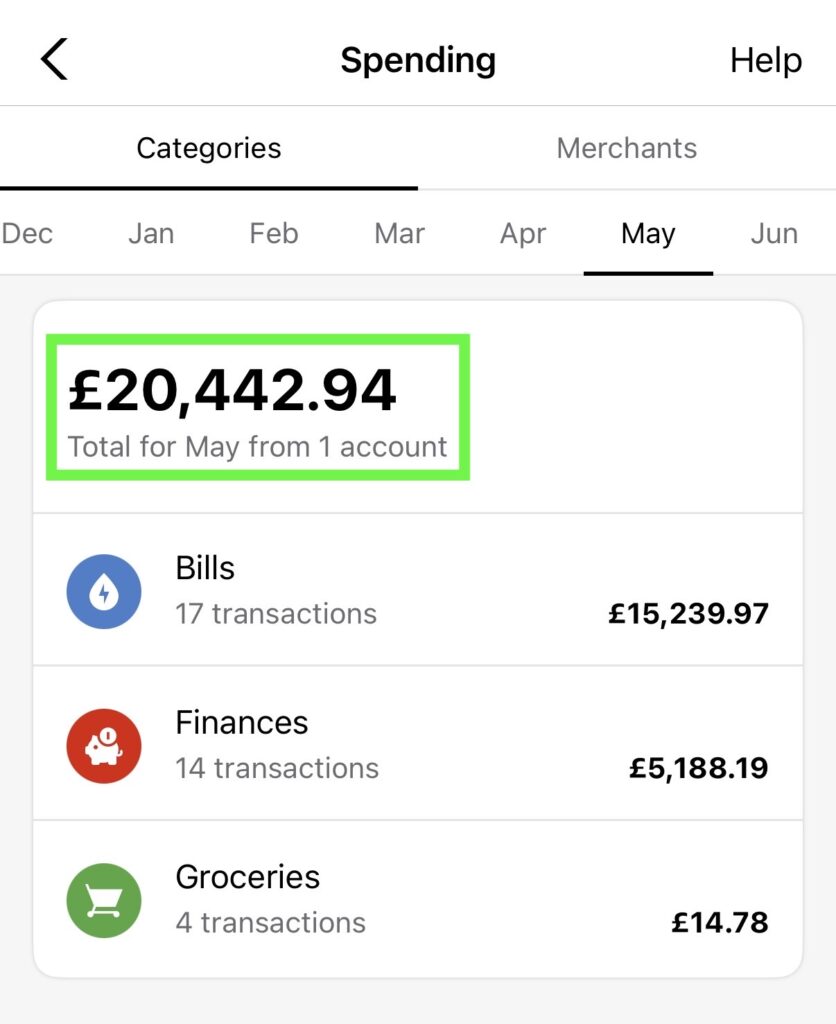

And if, like me, you care about seeing your spending clearly, there’s a catch: First Direct doesn’t separate spending from moving money around. You can’t exclude certain payments, so transfers and actual spending all get lumped together. The result is a pretty distorted picture of what you’ve really spent.

Believe you me, I did not spend £20k a month! I simply moved my money into a new savings account.

So why do I still think everyone should have it on their phone?

The perfect “money manager” account

First Direct sits in a really unique position in UK banking. It has the speed and cleanliness of a fintech app, but the infrastructure and reliability of a legacy bank. You get access to HSBC branches and cash machines, but without the bloated experience, hidden fees, or painfully outdated apps.

That’s what makes it perfect as a central money‑management account — not your spending account, not your rewards account, but your money handler. The place your salary lands before everything else gets sent where it needs to go.

And if you’re self-employed, you can pay yourself into First Direct and go from there.

Why it works so well:

- Fee‑free spending abroad — it’s a must for a money manager account

- Fast, clean app experience — no lag, no clutter

- Minimal distractions — no endless offers, rewards, or gamified nonsense

- Proper Open Banking support — essential if you use modern savings accounts, investing platforms, or budgeting tools (most banks support open banking, but not all)

It quietly does its job better than almost anyone else.

How I’d use it

Imagine you earn £3,000 a month.

Your salary lands in First Direct.

From there:

- £2,000 goes to your personal spending account, maybe Lloyds

- £500 goes into savings, perhaps Spring

- £500 goes into investments, say Vanguard

So the flow looks like this:

First Direct → Lloyds (£2,000)

First Direct → Spring (£500)

First Direct → Vanguard (£500)

Your everyday spending account stays clean and easy to understand. No salary deposits, no savings transfers, no investment transactions — just your actual spending.

That’s how I use First Direct — Not as my main account, just the one handling the day‑to‑day mess quietly in the background.