I can’t get any of my friends excited about regular savers. The reaction is always the same: “What do I have to do? Do I have to save the same amount every month? Can I skip a month? Can I opt out?” And inevitably: “It’s just not worth it.”

I get it. Regular savers feel like they ask a bit more of you. They seem like something you need a strategy for.

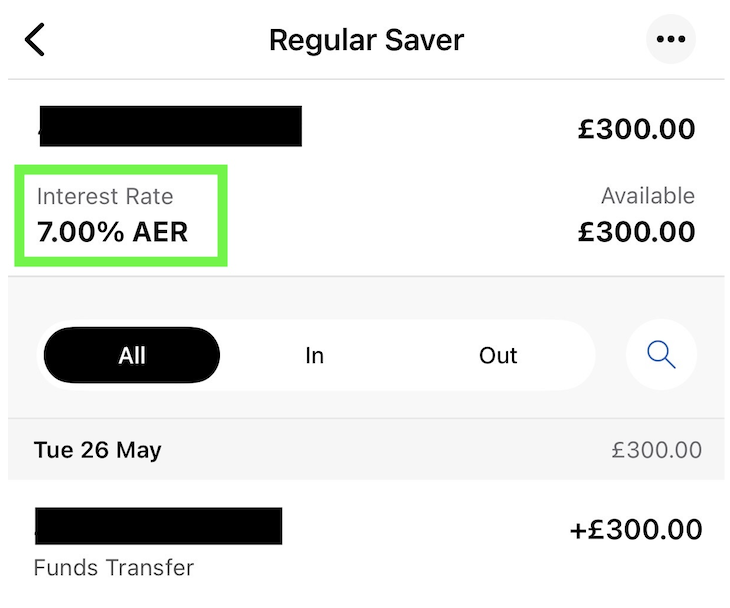

But before we get into any of that, let’s look at what a regular saver actually is — and whether you really get 7% with First Direct.

How does it actually work?

First Direct lets you save between £25 and £300 per month into a regular saver paying 7%. The important part is this: You only earn interest on the money for the amount of time it actually sits there.

So if you save £300 monthly for a year:

- In month one, you earn 7% on £300

- In month two, you earn 7% on roughly £600

- In month twelve, you finally earn 7% on the full £3,600

That means the average balance across the year is roughly half the final amount. Which is why the actual profit feels much closer to around 3.5% on the total money contributed.

Quick tip: whatever rate you see on a regular saver, the most you’ll actually make is just under half of it. So if you see a 6% regular saver, remember you’ll earn just under 3% at the end of the 12 months.

Let’s do the math

How the interest actually builds in a regular saver:

- 1st month: 7% (monthly) on £300 → £1.75

- 2nd month: 7% on £600 → £3.50

- 3rd month: 7% on £900 → £5.25

- 4th month: 7% on £1,200 → £7.00

- 5th month: 7% on £1,500 → £8.75

- 6th month: 7% on £1,800 → £10.50

- 7th month: 7% on £2,100 → £12.25

- 8th month: 7% on £2,400 → £14.00

- 9th month: 7% on £2,700 → £15.75

- 10th month: 7% on £3,000 → £17.50

- 11th month: 7% on £3,300 → £19.25

- 12th month: 7% on £3,600 → £21.00

You can see how it works: just keep adding the £300, and each month the growing balance earns a little more interest than the one before.

Total maximum interest: £136.50

Total deposited: £3,600

Total at the end: £3,736.50

So is the First Direct 7% account worth it?

It depends on what you want from it.

If you’re expecting a loophole into a 7% savings account when most people are getting 4% at best, you’ll be disappointed. But if what you really need is a bit of structure — something that automates your saving and treats it like a bill that gets paid every month — then it’s a win‑win. You build a habit that actually sticks, and you get the highest rate on the market for doing it.