Once you get used to products that stay out of your way and actually fit your life, it’s hard to put up with the other kind. Suddenly the noisy, over‑engineered ones stand out — the ones that add friction and then charge you for the experience.

My favourite products at the moment are Chase and Lemonade Insurance. Spring Savings is another (yes, even with that silly dog.) Those apps are all signal, no noise.

On the other end of the spectrum, there’s Revolut. Tiered subscriptions, a new card design every two seconds, wallpapers, thirty app icons, crypto, RevPoints — it’s everything I want to cut out of my finances. The endless gamification, the constant nudges, the sense that the app is trying to get your attention at all costs.

And then there’s Plum, which somehow manages to take all of that noise and turn it into a business model.

So what is Plum?

According to Plum, it’s meant to be a kind of intelligent money platform — tracking your finances, nudging you to save, shifting spare cash into pots and products, all under the banner of helping you “build wealth effortlessly”. Okay then, let’s put that to the test.

I thought I’d start with the simplest product in the world: an easy access savings account. No investments, no ISA complications, no notice periods, no withdrawal limits. Just a place to put money and earn the best interest you can.

What does the market offer right now? Easy access accounts paying around 3.75% AER are hardly difficult to find. Marcus offers 3.75%, while Cynergy, Post Office, Cahoot and others regularly push beyond 4%. My own savings are with Spring at 4.30% AER (with a bonus for a year). None of these companies are on a mission to “maximise wealth”. They’re just offering savings accounts.

So I was curious to see what Plum had in mind.

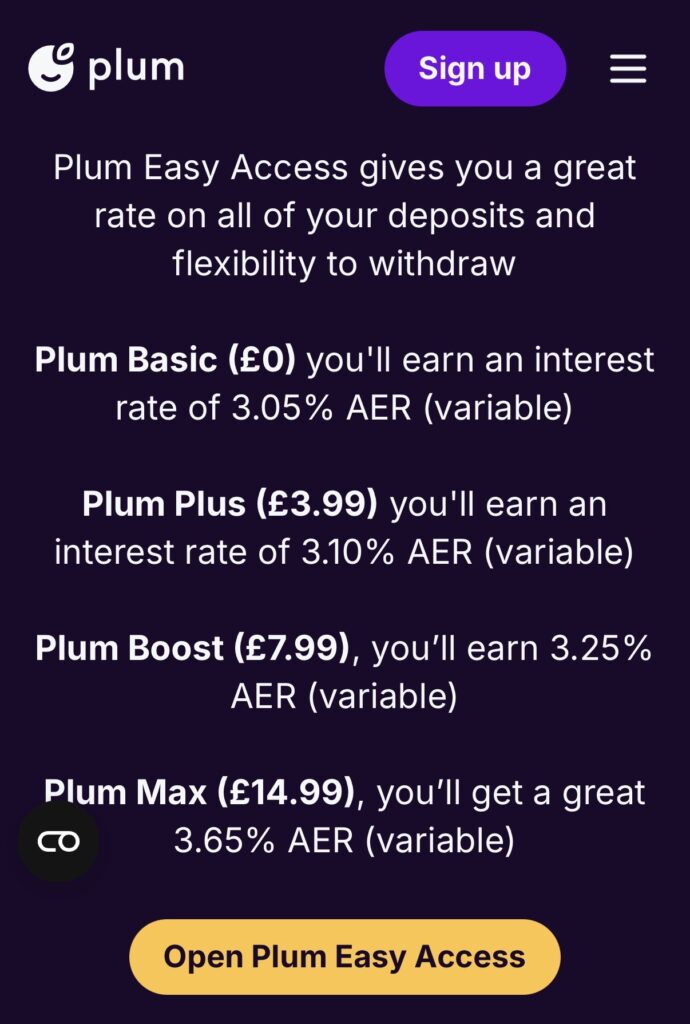

Plum’s savings accounts

Plum Basic (free): 3.05% AER

Plum Plus (£3.99): 3.10% AER

Plum Boost (£7.99): 3.25% AER

Plum Max (£14.99): 3.65% AER

The lowest rate on my list was Marcus at 3.75%, completely free, with a dedicated app. Plum wants you to pay £14.99 a month for the privilege of earning 3.65%.

Where do you even go from there?

The answer is simple: far, far away from products like these.

And here’s the sad part — maybe they really do have something with all the AI and automation. Maybe some people genuinely struggle to save and a fun app taking charge is exactly what they need. Let’s grant that.

It still doesn’t matter. When a company tries to pass off below‑average rates as part of a MAX or PLUS tier that costs £14.99, I’m running in the opposite direction. Their best offer — the one with the premium price tag — doesn’t compete with seven or eight free accounts I can list off the top of my head.

Bottom Line

Part of me wanted to download the app, poke around, see if there was anything clever inside. But I’m not going to. I don’t need to know whether Plum is good at investing. The fact that it asks me to pay for worse savings rates tells me everything I need to know about whether I want it involved in my finances.