I’ve had Monzo as my personal bank account for years. Or at least as one of them. As a recovering optimiser, I played the game fully: switch rewards, juggle six to eight accounts, take a bite out of each. It was fun for a long time, until it wasn’t. At some point the effort wasn’t worth it anymore.

These days I only keep one fintech bank for personal use, and that’s Chase. But for business, Monzo is the ideal fit. Here’s why.

The Monzo business app

Before I walk you through the practical benefits, let me get the obvious one out of the way: that little ka‑ching when money hits your account is priceless. Sometimes I think banks forget how much the small things matter, how the tiniest detail can change the whole feel of using an app.

So yes, Monzo is still the king of notifications. No one is faster, clearer, or more consistent. The categorisation makes sense without becoming the endless menu you get in Starling. Income is unmistakable: bright green, large font, a positive vibe. It changes the emotional feel of the app in a way that’s hard to overstate. Monzo is just fun to use.

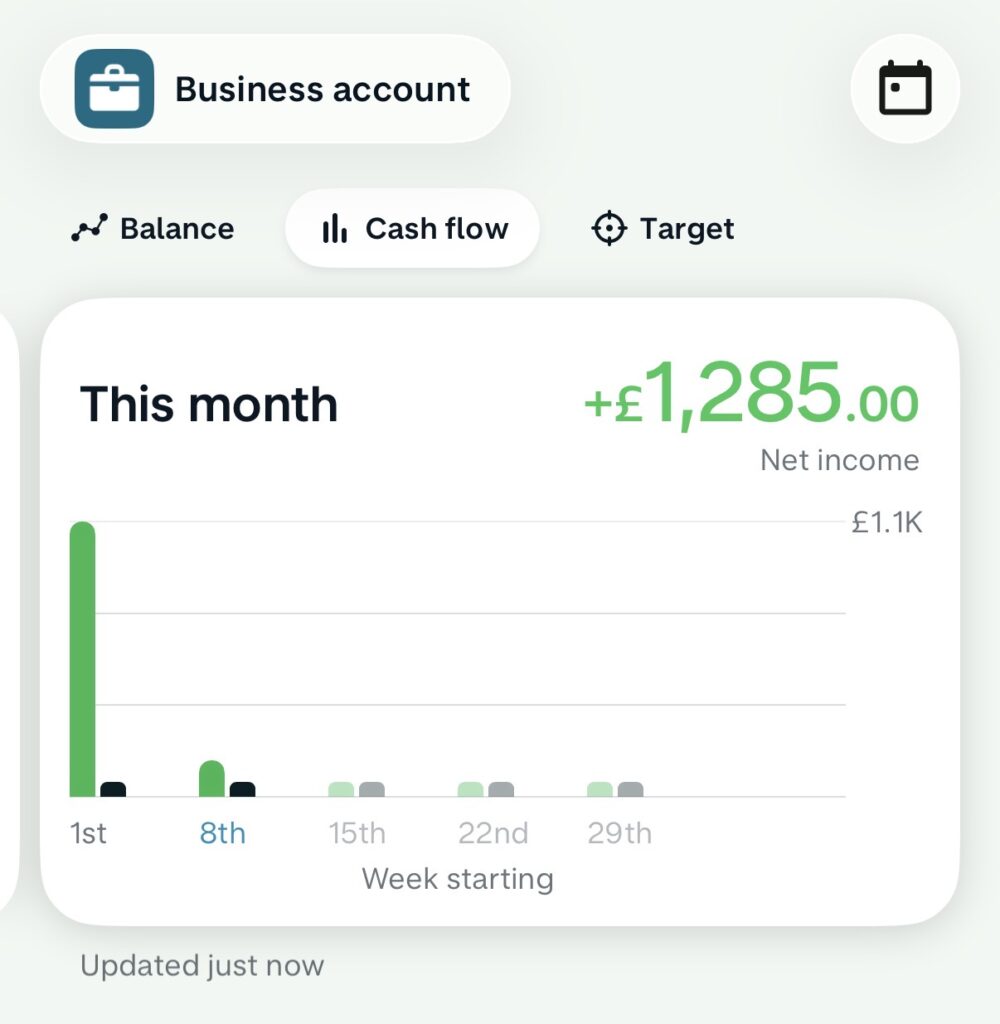

What else? The monthly view, the annual view, the tax‑year view — Monzo just does this better than anyone. Every client or merchant you’ve ever dealt with sits there with their full payment history. Every date, every amount, the averages, the patterns. And you can search, filter, and sort it in more ways than you’ll ever actually need, but it’s all there instantly when you do.

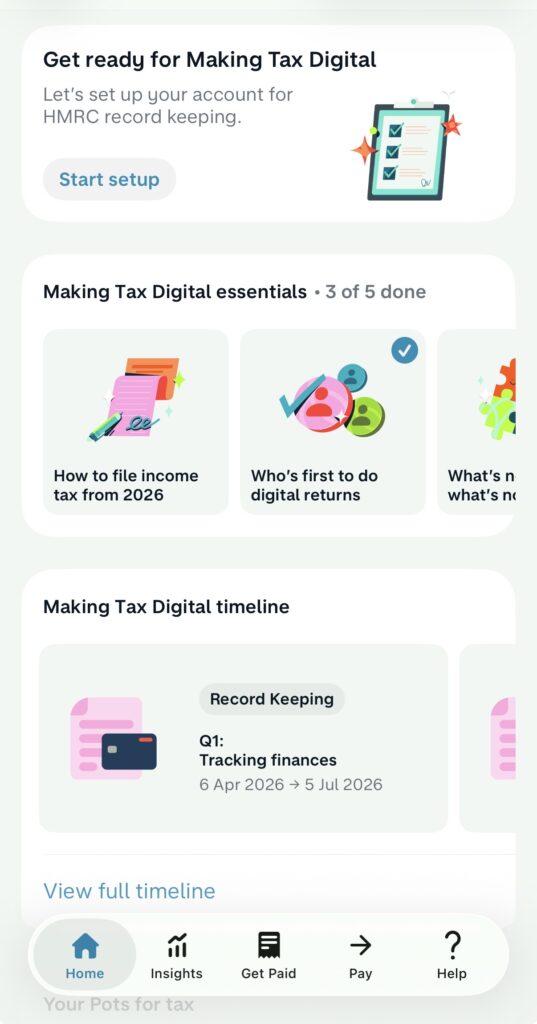

And looking ahead, Monzo has been the quickest and clearest about how Making Tax Digital works, what’s coming, and what you need to do. Starling is also free, apparently, but their messaging hasn’t had the same clarity. Monzo gives off the sense of we’ll make this as easy as humanly possible. A kind of just click here and you’re done.

What about the competition

For a sole trader like me, the requirements are basic but very specific. I want speed, visibility, reliability, ease of use, and a business account that’s genuinely free. I want the bank to feel like a partner in seeing my finances clearly and setting me up for MTD, not another thing I have to manage.

Realistically, the competition looks like Tide, Mettle from NatWest, and Starling. Tide charges a fee for every transfer, so I never seriously considered it. Mettle feels cold and corporate, exactly the sort of product a big bank would produce. And I’m not convinced it’ll stay free in the long run. So it always came down to Monzo or Starling for me.

I had the Starling business account for a while. I kept it dormant just in case, but unlike with the personal account, I couldn’t find a single area where Starling felt better than Monzo. It’s simply a case of Monzo being slightly better at everything. A bit more intuitive, a bit clearer, even colour‑coded in a way that makes more sense. The Monzo design just works better for me.

Final thought

So in the end, it wasn’t all that close. Monzo was an app I already knew well, it handled the business side of things better than anyone else I tried, and it’s the clear front‑runner on MTD in terms of how they prepare you for it. No one knows yet who’ll handle MTD best, or whether the differences will even matter, but at some point you have to go with your gut. Who do you trust. And my gut says Monzo.