First thing’s first: I love Amex.

I still remember how excited I was when I got my first Amex card. It was the Basic Card — it didn’t even work with Apple Pay at the time. And yet I was genuinely happy to be part of the “club”.

Over the years I moved through the cashback, Avios, and reward cards. I took advantage of the introductory 5% cashback offers, collected Avios for a while, and eventually scaled down to simple MR points.

I’ve had a great experience with the brand. Customer service has always been excellent, and I’ve genuinely had zero issues over the years.

So what’s changed?

I’m in a different phase

I don’t want to count points, chase rewards, or let a card decide what I order or where I go for dinner. It was fun for a long time, and I genuinely enjoyed it, but I don’t want to live like that anymore.

Am I just getting older? Probably.

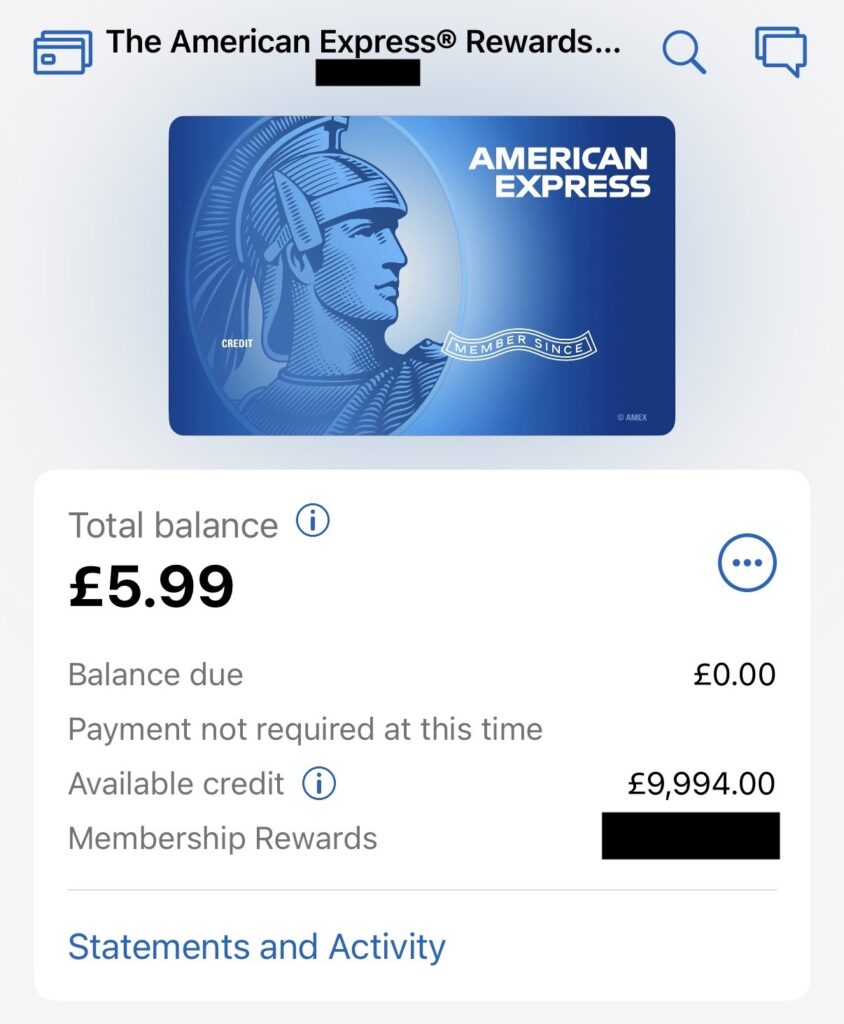

At some point, Amex stopped feeling like something that helped me and started feeling like something I had to justify. Even the high credit limit I once chased now feels more like an inconvenience.

And if I’m done playing that game, why do I need a card that isn’t even accepted everywhere?

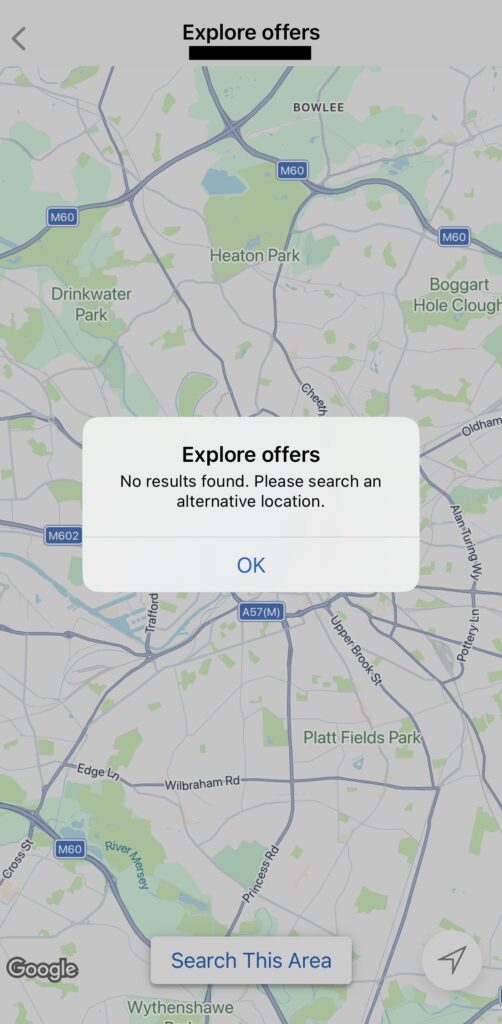

Acceptance is still an issue

There are also practical reasons.

Offers have weakened over time — fewer dining deals, lower cashback, and less of the value that made the Amex ecosystem fun in the first place.

And for all the improvements in acceptance, it still isn’t a Visa or Mastercard in the UK. At some point, you just want to pay for things without checking whether a place takes Amex. That everyday friction adds up more than you think.

There’s no way around it – it’s become a bit of an ick.

But that’s me. For the right person, Amex still does exactly what it promises. If you’re deep in the Avios ecosystem, there’s probably no better partner card. If the Gold card benefits make sense to you and how you naturally spend, then by all means go for it.

Three options if you’re ready to move on from Amex

If you’re feeling the same shift I did, here are your options:

Keep it as an emergency card

Let it sit quietly on the sidelines. Put a recurring bill on it — Netflix, Spotify, anything low‑maintenance — and otherwise forget about it. Think of it as your emergency card: one that’s there if you ever genuinely need it, without demanding attention the rest of the time.

Reduce the limit

If you’ve got a five‑figure limit but barely put a tenner through it each month, trim it down. A £1,000–£2,000 limit is more than enough for a couple of bills, the odd purchase, and the occasional worthwhile offer. There’s no prize for maintaining a huge limit you don’t use. We’re not trying to impress the credit score algorithm.

Say goodbye

Financial products are meant to serve you, not the other way around. If you’re constantly finding reasons to use the card — or reasons to keep it open — that’s usually a sign you’ve outgrown it. Closing it just means you’re done with it — nothing more. It’s recognising that your needs have changed.

What I want instead

I’m trying to simplify things.

A default card in Apple Pay that just works everywhere, without the little decisions or background optimisation running every time I pay. No mental load. No system to look after. Just spending when I need to and getting on with my day. That matters more to me now.

I still like the straightforward stuff: a bit of cashback, a clean offer, something that just works without asking anything from me.

What I’m not interested in anymore is a points system that needs managing, or one that nudges me toward certain shops or certain spending just to make the maths work. The kind of rewards I value now are simple, predictable, and don’t guide my behaviour. Just a nice extra when it happens.