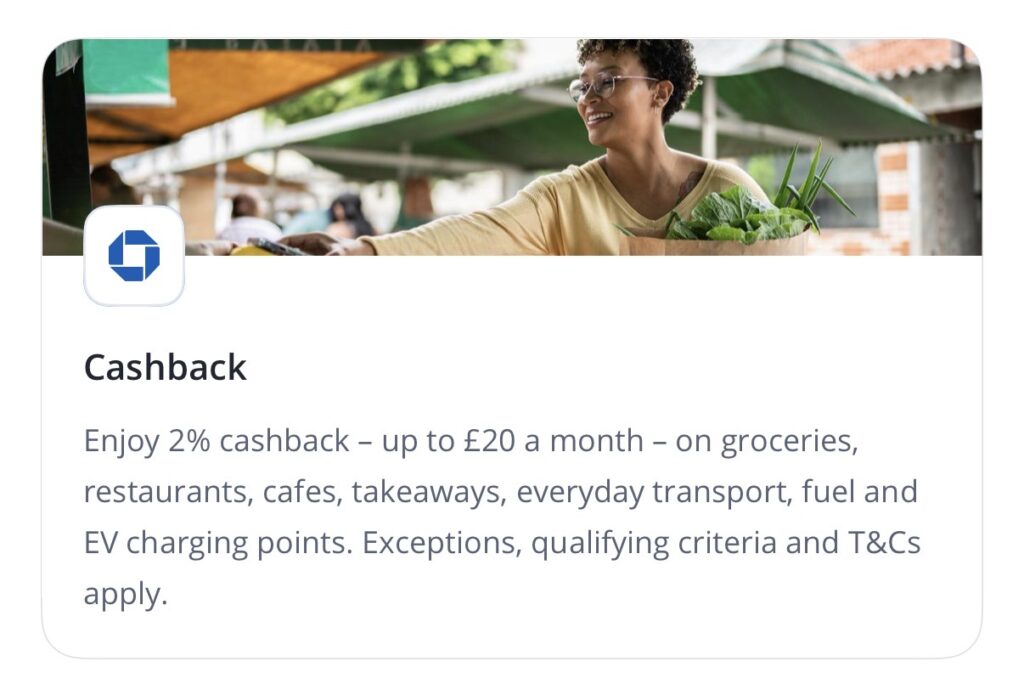

Chase has just launched a 2% cashback offer — which is pretty unusual in UK banking for a straightforward, everyday cashback deal. In the US, offers like this are far more common, so it’s no surprise it’s coming from the American giant.

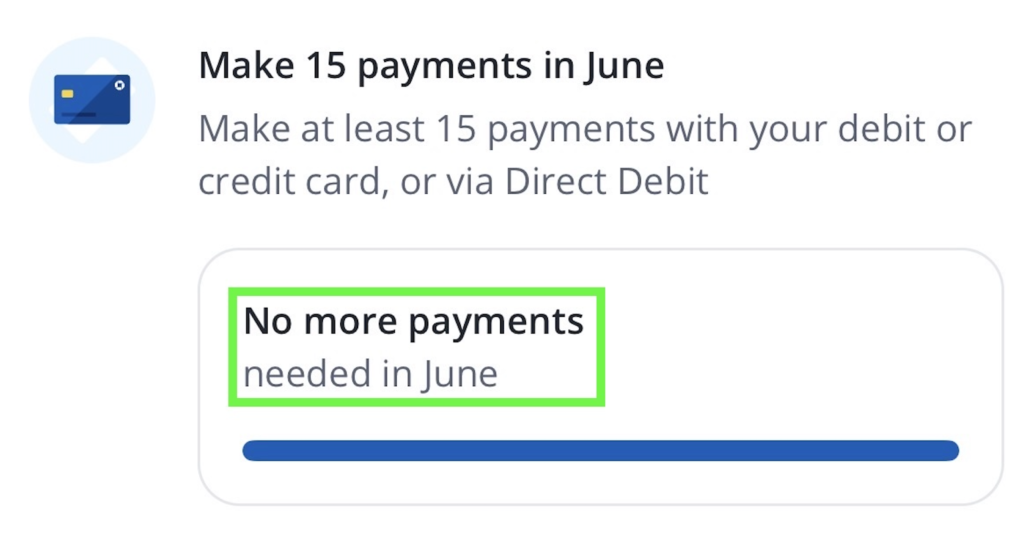

It’s practically no strings attached, although there are a couple of conditions in June you need to meet to qualify in July:

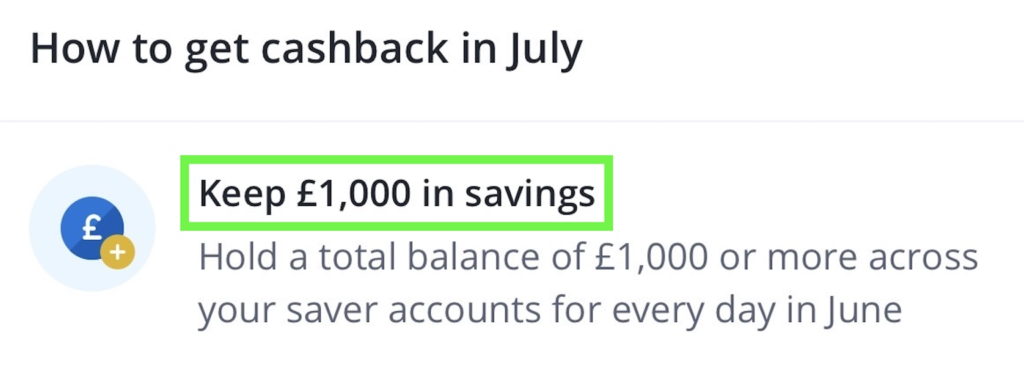

- Keep at least £1,000 in savings with Chase every day of the month

- Make 15 payments using either your debit card, credit card, or Direct Debits

Once that’s done, you’ll start earning cashback from July 1st onwards.

The categories are pretty straightforward. Basically anything to do with food and travel:

- groceries

- restaurants and cafés

- takeaways

- everyday transport

- fuel

- public EV charging

How you can actually use this

There are two ways to approach this offer:

1. The simple approach

Since Chase covers the majority of everyday spending, you can just make it your main spending card — or even your only card. Make it your default on your phone and just live your life. No optimisation, no overthinking.

You’ll probably hit the 15‑payments requirement without trying. And even if you don’t track it manually, the app does it for you. The benefit here isn’t just cashback — it’s zero decision fatigue. One card for most or all spending.

2. The optimised approach

If you want to squeeze more value out of it, you can split spending: use Chase for the 2% categories, and use another card for everything else (like an Amex or a different rewards card).

That way, the bulk of your spending gets rewarded through Chase, and whatever doesn’t fit their categories still earns something useful on the other card. A little extra admin, but I think it’s worth it.

How I’m using the 2% offer from Chase

Right now I’m in my first year with the Lloyds Ultra credit card, which gives me 1% cashback on everything. I spend about £800 a month, and roughly 75% of that is food or travel — which happens to fall neatly into Chase’s 2% categories.

So my setup looks like this:

- £800 total spend

- £600 on Chase — earning 2%

- £200 on Lloyds — earning 1%

- Plus the occasional Lloyds offer at 5–10% (B&M, TK Maxx, that sort of thing)

That works out to £12 from Chase and £2 from Lloyds each month.

£14 a month is £168 a year.

That puts me at an effective 1.75% return on everything I spend over the year. Not bad for spending exactly as I normally would, with almost no strings attached.

One thing to note

Your eligibility works a little differently under the new cashback offer. With the old 1% deal, paying in £1,500 was enough to qualify for next month’s cashback. Now, you only qualify at the end of the month — because one requirement is holding £1,000 or more in savings every single day of that month. Not a terrible inconvenience, just something to keep in mind.

Final thought

This Chase offer is a clear winner in my view.

Mostly because it doesn’t ask much of you. No Direct Debits to set up, no switching bribes, no minimum salary requirements. Just a simple expectation that you use the card meaningfully — 15 times a month — and keep a modest amount in savings with them. For what you get back, that feels more than fair.

If you want to check the details for yourself, you can have a look on the Chase website.