When Chase launched its credit card in the summer of 2025, I was probably one of the first people to apply. I hit the button the second the invite appeared in my app. The whole thing was instant — approved, the credit card section just popped into the app, Apple Pay ready. Everything with Chase just works.

Given we’re talking about one of the biggest banks in human history, I was expecting an above‑average limit. If you hand out £1,000 limits, you’re not exactly inspiring people to use the card. But I wasn’t prepared for what came next: “your limit is £10,000”.

I remember being excited at the time. Now it mostly makes me laugh.

What does a £10k limit actually mean?

On paper, it’s just the amount a bank is willing to let you borrow. In reality, it’s how they see you: your income, your credit file, your existing debts, your utilisation, your internal score with the bank. Your actual relationship and track record with them. So even though Chase didn’t have lending products at the time, if someone has five figures in savings, some investments, pays a bunch of direct debits, and basically lives out of their debit card — those are all green flags.

So, yay for me. £10k limit.

But how useful is it, really?

For some people, very. If you’re a big spender, a traveller, someone who books whole trips in advance, a high limit makes sense. If you treat a high limit as an emergency card, that can make sense too. And, you might even see it as something to grow into. Maybe you’re a £5k person today, but you expect to earn more, spend more, and that’s before we even factor in inflation.

All of that sounds reasonable enough, but none of it applies to me.

I’m not a heavy spender. I have a fully funded emergency fund. I have more than enough credit elsewhere. So while I can’t think of a single benefit to a £10k limit, I can think of a few things that make me uncomfortable.

Why do people reduce their limits?

There are good reasons. Some people are tempted to overspend, so lowering the limit protects them. That’s definitely not me. Others worry about fraud exposure on a high‑limit card — and honestly, so do I. Why would I want a £10k card floating around the internet? Yes, you’re protected in different ways, but it still feels off.

In any case, that’s not the main reason. Mine is much simpler, and much more personal. It may sound silly, so bear with me.

£10,000 just doesn’t reflect my life. My spending, my habits, my needs.

There’s a heaviness to living out of sync with your financial products. That’s been one of my big realisations over the last few years, and a big part of why this blog exists. A £10k limit felt like noise. Something to manage, to justify, to make use of. Something I had to be “worthy” of.

Weird questions kept nagging at me: am I spending enough? Will they reduce my limit if I don’t?

I started thinking about a minimum spend I should hit. Like “definitely no less than 1%” but ideally 3–4%. At one point I even moved some bills from my current account to the credit card just to beef it up a little. It didn’t happen overnight, but eventually something just snapped and I thought: okay, this is ridiculous. This limit isn’t for me.

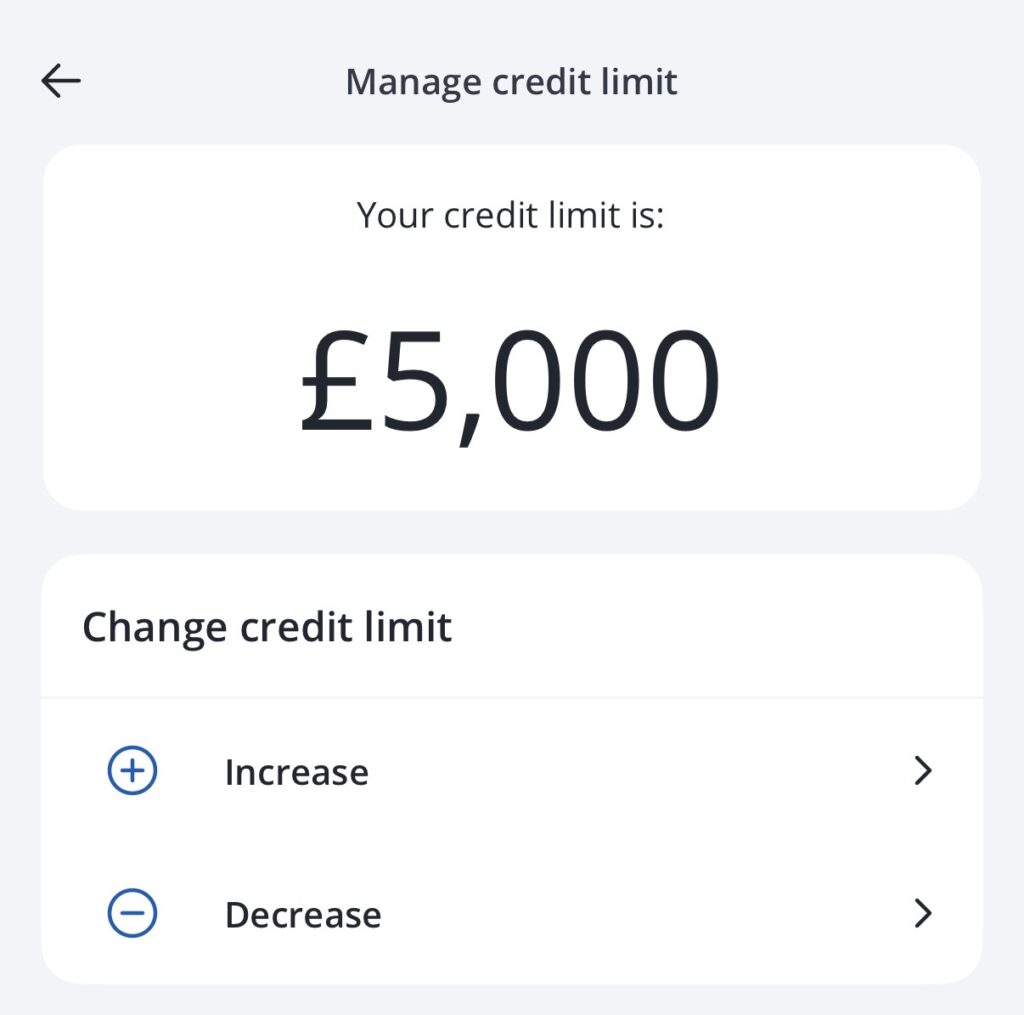

So I cut it in half to £5k, which means I can spend freely on the card and never worry about utilisation or overspending. And crucially, I don’t have to worry about underspending on it either.

There’s something freeing about picking your own limit. The right limit for you. It’s such a relief when it finally aligns with your actual spending. It just fits.