Most people assume their credit score does all the work.

If they’ve got excellent scores across all three CRAs — Experian, Equifax, TransUnion — they think they should automatically get any product they apply for. Umm… no. It doesn’t quite work like that.

Once you already hold a product with a bank, they often have something more useful than a credit file: direct experience of you. They can see how much money sits in your account, how you spend, whether you save, whether you invest, and whether you consistently bring in more than you send out.

That internal picture is often more valuable to a bank than a generic “account in good order, no late payments” on a credit report. That line could describe someone who barely uses their account at all. It tells them relatively little beyond the fact the person isn’t in trouble.

How to improve your internal bank score

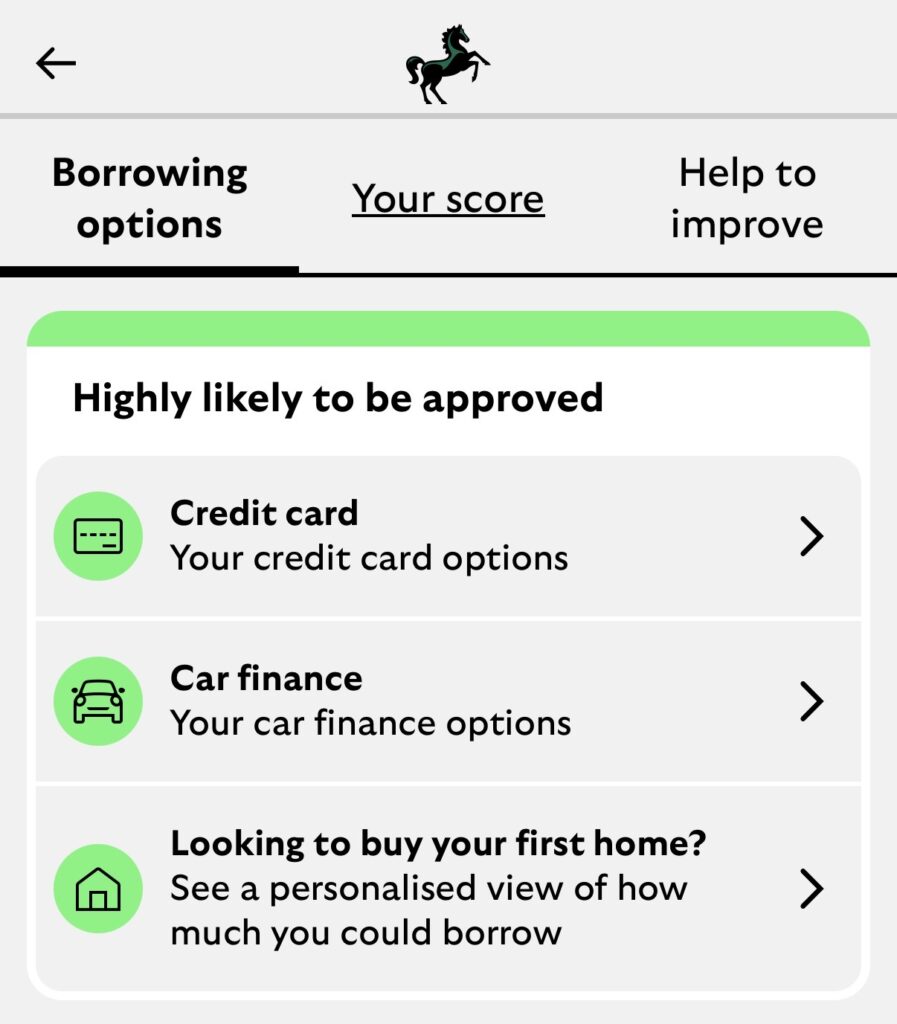

If you’re struggling to get a credit card with a particular bank, ask yourself two things: Do I actually have a relationship with them? And do I have a relationship with another bank in the same group?

It’s also worth understanding that a lot of UK banks aren’t really standalone in the way people assume. Many of them sit inside banking groups and can share data about you.

For example:

- Lloyds, Halifax and MBNA sit under Lloyds Banking Group

- NatWest and RBS sit under NatWest Group

- HSBC and First Direct sit under HSBC Group

So if you’ve got a Halifax account you barely touch, don’t be shocked if Lloyds or MBNA aren’t exactly rushing to approve you. Your internal bank score is often more meaningful to them than your external credit score, and each bank calculates it slightly differently.

And there’s really just one reliable way to improve it: use the account meaningfully.

What banks actually want to see

Back to our imaginary Halifax account. Say you haven’t used it in months, and you’ve got your eye on the new Lloyds Ultra credit card. The easiest thing you can do is make Halifax your main account for a month or two and see how your chances improve.

- Salary in

- Bills out

- Groceries

- Eating out

- Shopping

- Netflix

- Gym

- Keep a reasonable balance

That alone is often enough to start shifting how the bank sees you. If you want to go all out, you can add savings and investing products, but honestly it’s not necessary. Just live in that account for a while and don’t overthink it.

I did this myself a few years ago. I made Barclays my everything account and assumed it would take three to six months — these systems are famously slow. In the end, it took about a month. My internal score improved, and the credit card offer appeared with a way higher limit.

Final thought

If you’ve got strong credit scores, this whole thing can feel a bit baffling. The banks that don’t know you offer you everything, and the one that does says no. But there’s really no mystery here — the banks are just looking at different bits of information.

All you really need to do is show them you handle money sensibly. Honestly, that’s fair enough.