Writing about Club Lloyds made me think about the other reward accounts — the ones that sit in that middle space between free current accounts and the pricier packaged ones. They usually follow the same formula: a small monthly fee that gets refunded if you meet a couple of simple requirements, like paying in a set amount and running two Direct Debits.

The other offers are all structured differently, but each one has an obvious strength: Lloyds gives you lifestyle benefits (cinema tickets, Disney+ for a year), NatWest gives you straight‑up cash for using the account, Barclays builds its offer around an Apple TV discount, and Halifax focuses on interest — 3% at the time of writing. Santander is the only one where the numbers just don’t add up.

What do you get with Santander?

Santander Edge

- 1% cashback on household bills (up to £10/month)

- Fee‑free overseas spending

- Arranged overdraft available (subject to status)

- Requirements: £500 paid in each month; two Direct Debits

- Fee: £3

Cashback on bills

On paper it looks fine. Once you lay it out, you realise how much of it is just you trying to get back to zero. You pay a fee, you meet the requirements, and you only earn cashback on household bills. Every month starts the same way: you’re £3 down, and you’re already working to break even. It never feels like you’re getting ahead — it feels like you’re playing catch‑up with your own bank.

Compare that to NatWest’s offer: the requirements are simple and the rewards are predictable. Meet the conditions and you know exactly what you’re getting back each month.

Travel card

The travel card is useful, but it’s not a premium feature — you already get fee‑free spending abroad with Lloyds and Halifax for free, and the same goes for the fintech crowd as a whole. It’s a nice perk, just not one that justifies paying a monthly fee.

Arranged overdraft

Santander includes an arranged overdraft, but this isn’t a meaningful perk — almost every UK current account offers one. It’s basically business as usual, not a reward. You still have to apply, you’re still assessed on eligibility, and the rates are broadly the same across the high‑street banks. It’s useful if you need it, but it’s not something you’d ever choose an account for.

Let’s do some math

Okay, so let’s run some average household‑bill figures and see how quickly this offer falls apart.

Council tax: £150

Electricity & gas: £125

Broadband: £30

Water: £35

Mobile: £15

That all comes up to £385 per month in bill‑type spending that Santander counts.

What does this earn you?

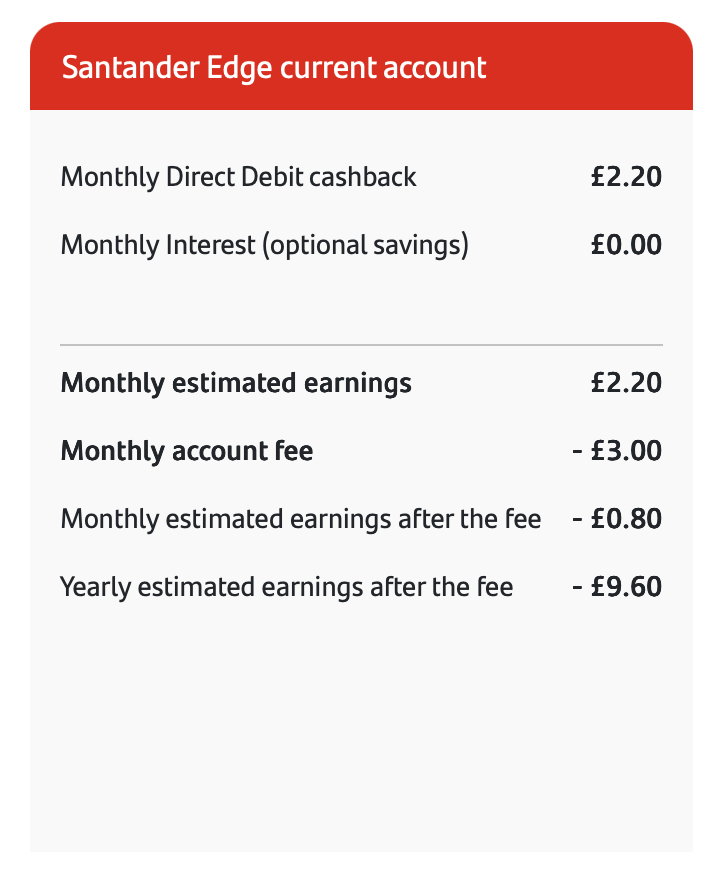

Cashback earned: £3.30

Fee: £3

Net gain: 30p

You’re doing all that… for thirty pence.

I then ran my own numbers and it gets even worse: I’m down 80p for the month, which works out to a £9.60 loss over the year.

So who’s this offer for?

For most people, Santander Edge only starts to make sense once their monthly bills are above £600. That’s the point where 1% cashback finally clears the £3 fee and leaves you with anything more than pennies. Below that, you’re spending the whole month trying to earn back the money you already handed over.

Bottom Line

Santander’s offer looks appealing at first, but the maths just doesn’t work. Every other bank has a clear strength you can point to; Santander is the odd one out. Once you factor in the fee, the hoops, and the standard features masquerading as perks, there’s very little value left for the average customer.

If you want to see the numbers for yourself, try it out with their own cashback calculator.